Upgrade to High-Speed Internet for only ₱1499/month!

Enjoy up to 100 Mbps fiber broadband, perfect for browsing, streaming, and gaming.

Visit Suniway.ph to learn

The Philippine Stock Exchange (PSE) has now put its own language on the Lopez cousins’ war. In a Publication of Penalties notice dated July 9, 2026, the exchange sanctioned First Gen Corporation for breaking the rules that govern what a listed company must tell the investing public, and when. Eight separate provisions, by the exchange’s own count. What began as a fight over power and loyalty inside one of the country’s most storied business families has produced a formal penalty against a listed company for falling short of rules designed to protect investors, not cousins.

At the heart of the controversy the PSE sanction now touches is a 3-part structure that First Gen, under chairman and CEO Federico “Piki” Lopez, built with the country’ richest man, Enrique Razon, and its biggest bank, BDO Unibank: the sale of a 60% stake in its gas business to Razon-led Prime Infrastructure for an agreed P50 billion (adjusted to P48.8 billion at closing); an investment in Prime’s pumped-storage hydropower projects, announced on February 13 as roughly P75 billion for a 40% interest and signed in March as a 33% interest worth about P62 billion; and P24.75 billion in committed BDO financing supporting the hydro acquisition.

All three instruments carry change-of-management triggers tied to Piki’s continued leadership. Two of them allow Prime to require First Gen to sell its remaining hydro and gas stakes back at a 25% discount if he is removed, an exposure First Gen itself has quantified at approximately P23.5 billion, while the third allows BDO to declare a default that can cascade through the outstanding loans of the wider First Philippine Holdings group, the parent of First Gen.

- Debt, discipline, and daring: Inside the Lopez Group’s high-risk bets

- The Lopezes, presidents, and the cost of dissent

- Lopez vs Lopez: The secrecy fight behind the Razon power deals

- How to make yourself very expensive to fire: The Lopez cousins’ war

This Rappler series on the Lopez cousins saga first traced that architecture in April (see list above), May and June (see list below), when it emerged that First Gen announced the hydro deal without initially telling investors that the change-of-management penalty structure sat in the fine print, information the market saw only weeks later, after the majority cousins went public.

- First Gen sat on a P23.5-billion Lopez clause for 60 days, then the family went to war

- Ceasefire on paper, war in the courts: Why the Lopez feud is far from over

- The business case of the Lopez-Razon gas and hydro deals

- [ANALYSIS] The Lopez ceasefire lasted only 26 days, then came the P50 billion math

The question then was simple: at what point does a P23.5 billion change-of-management architecture stop being a private comfort clause and start being material information the market is entitled to see? The PSE’s answer, written now in the language of Article VII and a published penalty, suggests the exchange has concluded that the timing and completeness of First Gen’s disclosures are no longer just a family grievance.

What the notice says, and what it does not

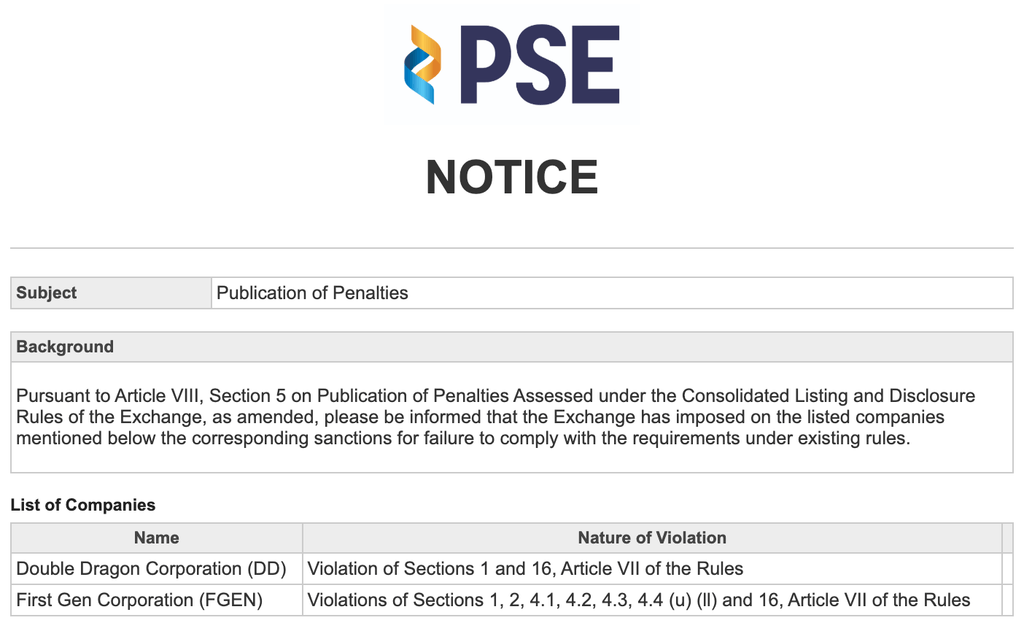

PSE’s July 9 notice of disclosure violations is terse. It is a routine publication issued under Article VIII, Section 5 of the exchange’s rules, and it lists First Gen alongside another sanctioned company that was cited for a narrower set of violations. The notice names the sections First Gen breached (Sections 1, 2, 4.1, 4.2, 4.3, 4.4 (u) (ll) and 16) but does not identify which disclosures triggered the sanction, does not state the amount of the penalty, does not specify the period covered, and does not say whether First Gen contested the findings or intends to appeal. Penalties for disclosure violations under the exchange’s rules typically take the form of fines. A story update will follow when more information becomes available.

Screenshot from PSE website

What the notice does provide is the exchange’s own checklist, and that checklist maps closely onto the disclosure timeline this Rappler series has documented:

- Sections 1 and 2 state the foundational duty: material information must be disclosed fully, fairly, accurately, and on time, and all investors must have equal access to it.

- Section 4.1 gives that duty a clock by requiring listed companies to disclose material information within 10 minutes of its occurrence.

- Section 4.2 prohibits communicating material non-public information selectively.

- Section 4.3 sets the test for what counts as material.

- Section 4.4 lists specific events presumed material, including board or stockholder resolutions approving material acts under paragraph (u) and the borrowing of significant funds outside the ordinary course of business under paragraph (ll).

- Section 16 imposes a separate and often overlooked duty: once a company learns that a prior disclosure was inaccurate or incomplete, it must correct or update that disclosure, again within 10 minutes. Ten minutes is the standard against which the roughly 60 days investors waited to learn about the P23.5 billion exposure must now be measured.

The citation of Section 16 deserves particular attention, because it speaks to a pattern this Rappler series has been tracking for months. First Gen’s original February 13 disclosure of the board meeting that approved the hydro transaction contained no mention of a change-of-management-control clause; that language appears only in an amended version of the filing dated April 2026. The company’s disclosure of the Definitive Agreements, first filed on March 9, was likewise amended on April 30 to describe the clause and to quantify the 25% discount at approximately P15.5 billion on the hydro shares and P8 billion on the remaining gas shares. Amended filings are how companies comply, belatedly, with the duty to update. They are also a paper trail showing what the original filings left out. If the exchange found a Section 16 violation, it may have looked at precisely that gap between the first version of the public record and the corrected one, though only the PSE can confirm which filings were at issue.

A second detail in the checklist is worth pausing on. First Gen’s most consistent public defense has been that it avoids the premature and selective disclosure of material information, precisely to protect equal access for all shareholders. Section 4.2 is the rule that prohibits selective disclosure. If the exchange has cited that provision against the company, then the rule First Gen invoked as its shield appears somewhere on the list of rules it was sanctioned for breaching.

Whatever the business logic of the deals, the PSE is saying the way the market was informed fell short of the standards it expects from a public company.”

Why the sanction changes the center of gravity

A family feud can be dismissed as private drama, but a disclosure sanction against a listed company cannot. The Lopez majority cousins, led by Eugenio “Gabby” Lopez and representing the three family branches that together hold 71% of private holding firm Lopez Inc., have spent months saying the market was told too late about multibillion-peso clauses tied to Piki’s continued leadership, while First Gen and Piki have spent those same months saying they followed the rules, protected equal access to material information, and did nothing wrong. The exchange has now entered with its own language, and that language is not about pain or betrayal or legacy but about continuing disclosure, board-approved material acts, and non-ordinary borrowings.

The sanction does not settle who should run the Lopez empire, does not prove every allegation raised by the majority, and does not erase First Gen’s defense that the clauses were commercially rational and board-approved. It does make one thing much harder to say with a straight face: that this was only a family quarrel. The exchange has marked it as a governance and disclosure problem too.

For a while the cousins’ war had a familiar script, with one side saying Piki had used corporate machinery to make himself expensive to remove and the other saying the majority was politicizing complicated commercial decisions and dragging a listed energy company into an internal power struggle. The penalties notice changes that script because it translates months of accusation and defense into a regulator’s own checklist, and a checklist is harder to argue with than a press release. Whatever the business logic of the deals, the exchange is saying the way the market was informed fell short of the standards it expects from a public company.

That gives the majority cousins something they did not previously have: an official, external foothold. It is not a final win and it is not control, but it is a regulator-backed signal that their complaints about the timing and completeness of First Gen’s disclosures now sit inside a formal compliance finding rather than a family grievance.

What the majority said, in its own words

The Lopez majority was not subtle when it went to the Securities and Exchange Commission (SEC) and PSE. In its April 22 press release, it said the two “poison pills” that kept Piki in place “were disclosed 6 months and 2 months late, respectively, in clear violation of stock market rules meant to protect the investing public by giving them full, fair, accurate, and timely information.”

The statement went straight to materiality, noting that the amounts involved were “roughly equivalent to a third or so of the market capital of First Gen” and “would affect shareholder dividends and eventually share prices if triggered.”

The rhetoric sharpened from there. “Do not claim to be an apostle of transparency,” the majority said, describing the management style behind the deals as “secretive” and insisting that if the market was to be protected, that style “should stop.”

Two days earlier, in its April 20 statement, the majority had already widened the frame, saying there were “two, not one as earlier discovered, poison pills” and that both were structured so that Prime would benefit while “the shareholders of First Gen are thrown under the bus.”

Its most memorable line was also its simplest: “So who is Piki working for?”

The April 20 statement pushed the accusation further: “Not content with selling away our gas crown jewel, Piki made sure he would remain on top — and relevant — but at everybody else’s expense. More than a lifetime’s worth of money owned by other people was put on the line all for one man’s job security. And it was all done in secrecy.”

Take away the family anger and what remains is a governance theory that other listed firms should pay attention to. If one executive’s continued role becomes the hinge on which billions of pesos of value can swing, that is material information. If the market learns about it only after insiders start fighting in public, something has already gone wrong in the flow of disclosure.

If the market learns about it only after insiders start fighting in public, something has already gone wrong in the flow of disclosure.”

What Piki Lopez and First Gen said, in their own words

First Gen and its chairman and CEO Piki Lopez did not answer these attacks meekly. They answered them as if the real issue was not concealment, but discipline.

In First Gen’s April 5 press statement, the company said it enters into contracts and agreements “only after conducting transparent and rigorous evaluations, and only upon thorough review and approval by its Board of Directors.” Then came the sentence that has become central to this entire fight: “First Gen, as a publicly listed company, observes with fidelity the rights of all stockholders to equal access to material information by avoiding its premature and selective disclosure, as mandated by law.”

The company noted that the Prime transactions were unanimously approved by a board that included both Piki and Manuel L. Lopez, cousins now in different camps of the war.

Piki used a similar register at his April 17 town hall with employees (see story below), calling the conflict “really a shareholder conflict,” telling employees there was “no need for you to take sides,” and describing the company’s management style as “rigid” and “regimented,” “even with regards to our fiduciary responsibilities.” He leaned on outside validation, referring to institutions like SSS, KKR, Macquarie, and Singapore’s sovereign wealth fund: “They would not be there, and they would not be as supportive if we did not manage our fiduciary responsibilities in the way that we did.” The clauses “being called in the press, the poison pills and the changes in management control,” he said, were provisions “being asked for by our partners” and by banks that “basically say that we got to stay here.”

Piki was not portraying himself as a man clinging to power. He was portraying himself as the executive that counterparties and lenders trusted enough to write into multibillion-peso agreements. In his telling, these clauses were not red flags. They were, in fact, endorsements.

At the May 28 annual stockholders meeting, First Gen president Giles Puno made the defense explicit. “Let’s be accurate and refer it, or if referred to it as either the change-of-management control clause or a key man clause,” he said, adding that the clause “was among the topics presented to, deliberated, and approved by the Board of Directors during its meeting in February 2026, prior to the signing of the head of terms agreement with Prime.”

Puno was careful to emphasize process. The board representative of KKR, the New York-based investment giant that holds roughly 20% of First Gen through Valorous Asia Holdings, he said, was present, as were the other directors, and the deal received “unanimous approval following several questions, clarifications, deliberations, and analysis among the directors.” He added that the provision was “widely recognized as a relatively standard contractual mechanism in the energy and infrastructure industries.”

Then he delivered the heart of the case: “As we have said, it was Prime, which requested the change of management control clause, as it clearly recognized the expertise of our chairman, Piki Lopez, as well as members of First Gen’s management team.”

Puno said Prime was “a relatively new entrant with limited experience in the operations and management of gas and hydro power facilities,” and that “the relationship between Piki Lopez and Ricky Razon, as well as those of their respective management teams, were a significant factor in Prime’s decision to partner with First Gen across the gas and hydro assets.”

That is the cleanest version of First Gen’s position, that the clauses existed but were negotiated provisions requested by a counterparty that wanted continuity, approved by a fully informed board, and handled within the company’s understanding of its disclosure obligations.

Where the two stories collide

Set the majority’s language beside First Gen’s and the collision becomes plain.

The majority said the information was “material” to the investing public and disclosed months late. First Gen said it protected “equal access to material information” by avoiding premature and selective disclosure. The majority said the clauses threw shareholders “under the bus.” Piki said institutions kept backing the group because of how it handled its fiduciary duties. The majority described the provisions as secrecy in service of one man’s job security. Giles Puno described them as a standard “key man clause” requested by Prime and approved by a board that had asked questions and deliberated.

The penalties notice matters because it does not decide which family narrative is morally superior. It does something more useful for investors by testing the competing stories against the exchange’s own rulebook. And at least at this stage, that rulebook did not fully accept First Gen’s self-description. If the company’s handling of the matter had satisfied Article VII, there would be no sanction to discuss.

Why the ‘equal access’ defense now has a ceiling

First Gen’s equal-access argument was always the strongest part of its public case. It had legal weight because once a company is listed, management cannot casually hand material nonpublic information to controlling shareholders, cousin factions, or favored insiders while everyone else remains in the dark.

But that argument has a ceiling. As earlier reporting in this Rappler series pointed out, the insider-trading shield covers the negotiation room, but it does not cover the filing cabinet. Once contracts are signed, material terms do not remain private simply because the subject is awkward, politically explosive, or tied to a family fight. They are supposed to become part of the market’s information set, within minutes rather than months.

This is where the PSE sanction strikes. By invoking Article VII, the exchange is saying, in effect, that however valid First Gen’s concern about selective disclosure may have been during negotiations, that concern did not excuse the company from its separate duty to disclose signed, material information to the market in a timely and adequate way.

That also weakens the rhetorical shield around the “vote of confidence” line. Maybe Prime did want continuity. Maybe lenders did see Piki as “necessary, vital and indispensable,” as First Gen’s earlier disclosure about the BDO financing put it. Maybe counterparties really did ask for key-man protection because they trusted the management bench around him. But a clause can be commercially understandable and still be under-disclosed to investors. One proposition does not cancel the other.

That distinction is easy to lose in a family war because everyone talks as if only one question exists. Was the deal good or bad? Was Piki justified or self-serving? Was the majority protecting shareholders or simply trying to take him down? The market asks a different question: Were investors told enough, soon enough, clearly enough, to judge the risk for themselves?

The part about borrowing that should not be overlooked

One of the more revealing details in the sanctions is the citation of Section 4.4(ll), the rule on significant borrowings outside the ordinary course of business, because this controversy was never only about the change-of-management clauses in the Prime contracts.

As earlier reported, First Gen disclosed on April 17 that BDO Unibank had issued standby letters of credit of P9.9 billion and P14.85 billion, a combined P24.75 billion, in support of the hydro acquisition, and that the financing came with its own change-of-management covenant. According to First Gen’s own disclosure, a Change of Management Control is an event of default in the outstanding BDO loans of the FPH group, triggered if Piki ceases to be chief executive of First Gen, if his designees lose their majority on the board and executive committee, or “if [Piki] and his family will cease to own directly or indirectly at least 29.17% of Lopez Inc.”

That is what made the architecture of the dispute so striking, because the issue was never one clause in one contract but a structure of three instruments across two counterparties with one practical effect: that removing Piki could become very expensive very quickly.

For ordinary investors, that is exactly the kind of information gap disclosure rules are supposed to close. Banks can protect themselves. They do due diligence, negotiate terms, and bargain from a position of strength. Public shareholders do not get that luxury. They see what the company discloses, when it discloses it, and they make decisions from there. That is why the PSE’s use of Section 4.4(ll) matters. It shows the exchange may have seen a wider pattern: not just delayed or incomplete discussion of a governance clause, but disclosure questions touching major financing that was not routine and that interacted directly with control risk.

First Gen’s posture ‘we did nothing wrong’ becomes harder to sustain in total, because the PSE has already said something in the disclosure chain did go wrong.”

What the sanctions mean in the cousins’ war

At one level, not much changes overnight. Piki remains chairman and CEO, the Prime deals remain in place unless other legal or corporate actions alter them, and the cousins are still fighting in other forums over the broader question of who should lead the Lopez group. At another level, a great deal changes. Before the sanction, the majority had a political and moral case that First Gen could answer with its own legal language about equal access and board approval. After the sanctions, the majority also has a regulatory echo. It can now say the exchange itself found Article VII violations. That does not prove every colorful charge in its press releases, but it makes those complaints harder to brush aside as mere theatrics.

For Piki and First Gen, the burden shifts. They can still defend the economics of the Prime transactions. They can still argue that key-man clauses are standard, that Prime requested them, that lenders and institutions backed their leadership, and that the board knew what it was doing. But they now have to make that defense with a formal market sanction sitting beside it. The posture “we did nothing wrong” becomes harder to sustain in total, because the exchange has already said something in the disclosure chain did go wrong.

What other family businesses should learn from this

Strip away the surnames and the inheritance wounds and the old money. What is left is a governance lesson other listed firms should study closely.

First, family conflict is not a private matter once it spills into material contracts. If leadership continuity is written into deal terms in a way that can move billions of pesos, then the issue is no longer just succession. It is disclosure.

Second, “key man” and “poison pill” are not mutually exclusive labels. A clause may genuinely be requested by a counterparty that wants continuity. It may also have the effect of making one executive extraordinarily difficult to remove. The market needs enough information to decide which description matters more.

Third, governance rhetoric is not self-executing. Phrases like “transparent and rigorous evaluations” and “equal access to material information” have to line up with sequence, and if the public learns the real dimensions of risk only after a family faction goes public and the exchange starts asking questions, the rhetoric begins to sound less like principle and more like cover, even if that was never the speaker’s intention.

And fourth, this is why disclosure rules exist. Most investors are not in the boardroom, the family, the negotiating room with Prime, or BDO’s credit process; they buy a stock, or hold it through a pension fund, and trust that the documents they receive are enough. The market works only to the extent that this trust is not abused.

That is the point at which the First Gen case stops being a Lopez story and becomes everybody else’s problem too. The cousins may be fighting over power, but the exchange, in its dry language, is testing whether the rules still protected the people outside the family circle.

That is the fight that outlasts this family. It is also the more important one. – Rappler.com

Lala Rimando wrote about Philippine business, and managed newsrooms, including Newsbreak, ABS-CBN, Rappler, and Forbes, for over 25 years. She’s now based in La Union, taking care of her mom with dementia, and working on the multimedia biography of the late John Gokongwei.

![[Newspoint] No more deals](https://www.rappler.com/tachyon/2026/07/NO-MORE-DEALS.jpg)