Upgrade to High-Speed Internet for only ₱1499/month!

Enjoy up to 100 Mbps fiber broadband, perfect for browsing, streaming, and gaming.

Visit Suniway.ph to learn

While our ASEAN neighbor Singapore has early on warned its citizens about the negative consequences of the Middle East conflict, and continues to regularly inform and its citizens the economic problems that will affect the island state, our own government officials, on the other hand, prefer to avoid warning Filipinos on the need to realistically look at their financial resources and prepare for our local economy to get progressively worse in the next few months if the US and Iran still cannot come to an agreement to end their conflict and finally allow global energy supplies to normalize and rebuild.

Even as I write this column, the government just officially announced that the April inflation has jumped to 7.2 percent from 4.1 percent in March and just 2.4 percent in February, just before Israel and the US started the war against Iran.

Singapore’s Prime Minister Lawrence Wong and its Foreign Minister Dr. Vivian Balakrishnan have taken to social media and credible news outlets to clearly warn and prepare their fellow Singaporeans about the economic repercussions from the continuing Middle East conflict even though the Singaporean government has clearly prepared for such economic headwinds and is fiscally able to weather persistent global economic headwinds.

Our government, instead of advising or advocating for realistic planning and preparation by Filipino families, continues to hype a positive outlook that appears to indicate that foreign investors, financial markets and private credit are ready to invest in the Philippines in spite of the global uncertainty.

Such positive posturing is the hallmark of Filipino governance: distract with promises, fall short of actual performance and continue deflecting with political intrigues and hocus-pocus.

Even before the Middle East conflict started, investment inflows into the Philippines were already sluggish. According to officially released figures, net foreign direct investment (FDI) in the Philippines in 2025 totaled $7.8 billion, a 17.1 percent decrease from the $9.398 billion recorded in 2024.

The 2025 FDI figure is the lowest level since 2020 and is attributed to global tensions and local governance issues. Intensified global tensions from the Middle East turmoil and the same local governance issues are still hounding the country and are not expected to be resolved any time soon.

The Philippines has also recorded a six-month high trade deficit of $4.5 billion in March. Exports surged 20.4 percent to $6.78 billion, while imports rose 12.3 percent to $11.29 billion. This means that we are not earning as much from our exported products and continue to rely on more imports from other countries. Less income inflow and more payments for the higher cost of imports due to a devalued peso.

The Middle East crisis is also affecting our reliable remittances from our overseas Filipino workers based in the conflict region, with the government even discouraging Filipino seamen from deploying abroad despite the continued demand. According to economist Jonathan Ravelas, in a recent briefing for members of the Nordic Chamber at the German Club in Makati, the government is actually discouraging Filipino seafarers from going abroad at this time because of the cost of possible repatriation from the Middle East conflict. The Philippine government, Ravelas said, is already fiscally strained.

The estimated cost of repatriating a single Filipino from the Middle East has nearly doubled to approximately P190,000 as of April 2026, up from previous estimates of P150,000 and earlier baseline costs of P100,000. The increase is primarily driven by rising airfares and increased insurance premiums linked to the ongoing regional conflict. To manage the higher costs and requests, government agencies have requested significant additional funding, with the Overseas Workers Welfare Administration requesting an additional P12 billion from the Department of Budget and Management. This request includes P9 billion for the emergency repatriation fund and P3 billion for reintegration programs.

The 2026 national budget initially allocated P6 billion for repatriation efforts, but officials warn this could be insufficient. There are estimates that if the conflict worsens and a larger portion of the 2.4 million Filipinos in the region requires evacuation, the total cost could reach P13 billion.

I don’t know why the government thinks that it can easily spin the economic downturn facing our economy with the Pax Silica initiative — a US-led, 14-nation coalition aimed at securing the artificial intelligence and semiconductor supply chain by establishing in the Philippines a 4,000-acre “AI-native” industrial acceleration hub in New Clark City that will focus on critical minerals (copper, nickel), manufacturing and technology to reduce dependence on rivals and enhance economic security — when such an ambitious investment plan would take years to plan, and even more years to materialize and actually show concrete benefits, and with the current government not even sure that it will still be in existence by 2028.

The government must not keep on misleading the people into thinking that it can rely on ayuda to tide them over this conflict that has now reached two months and is likely to fester for a longer period. And if by some miracle a sudden cessation is reached, getting back to business as usual would take a year or more.

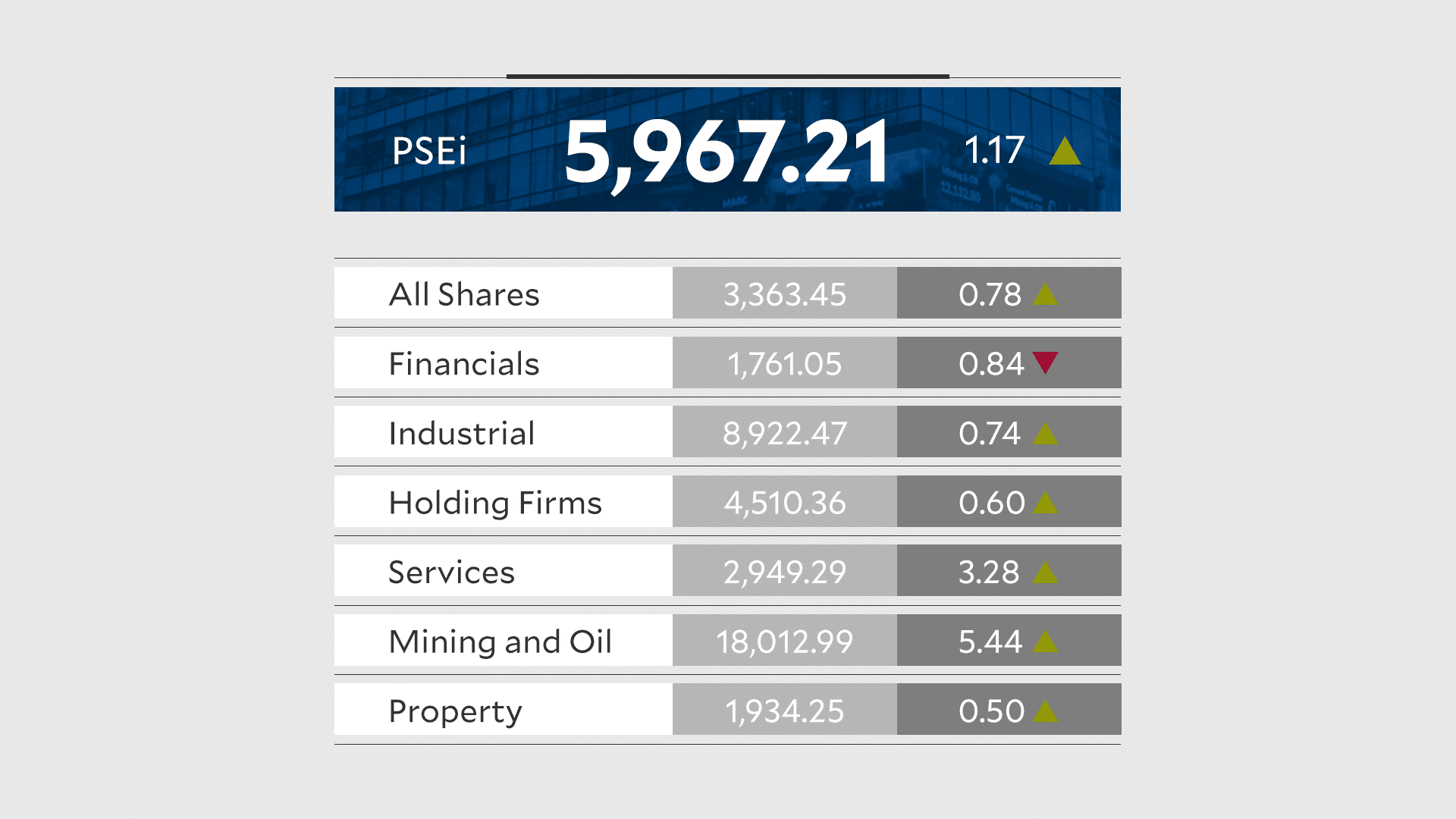

Additionally, our equities markets have shown that investors, both local and foreign, are truly pessimistic about the economy and investor confidence. Ravelas boldly advised during his briefing last week to “sell your stocks and run away.”

The Philippine Stock Exchange Index or PSEi has been trading below the 6,000 level and as of Monday closed at 5,942 and is likely to tank when the market closes today. (please update Tuesday closing).

The Peso to US dollar exchange rate has already deteriorated to P61.68-61.70 and is likely to weaken further during trading today.